Digital wallets began to emerge in the online and mobile ecosystems in the 1990s and have quickly evolved since then, with an expanding number of companies offering them. Meanwhile, the number of features offered is also increasing.

While PayPal was one of the first companies to create electronic money services, it didn’t develop a digital wallet for years. Other technology giants, including Apple and Google, have jumped into the ring too, making their wallets available with their proprietary software. More recently, newer players in the market, including Early Warning Services, have also introduced digital wallet products. The social media company X, formerly known as Twitter, is also contemplating a payments tool that may look like a digital wallet.

Even as some parts of the world, including certain countries in Asia, rely on digital wallets for payments online and in-person, consumers in the U.S. are still getting used to the idea.

That’s likely to change as more digital wallet providers compete in the U.S. market and the technology evolves. With more competitors jockeying to attract consumers, taking new approaches and offering fresh features, use of digital wallets in America is poised to grow too.

Below you'll find some of our latest Payments Dive stories on the fast-evolving digital wallet market.

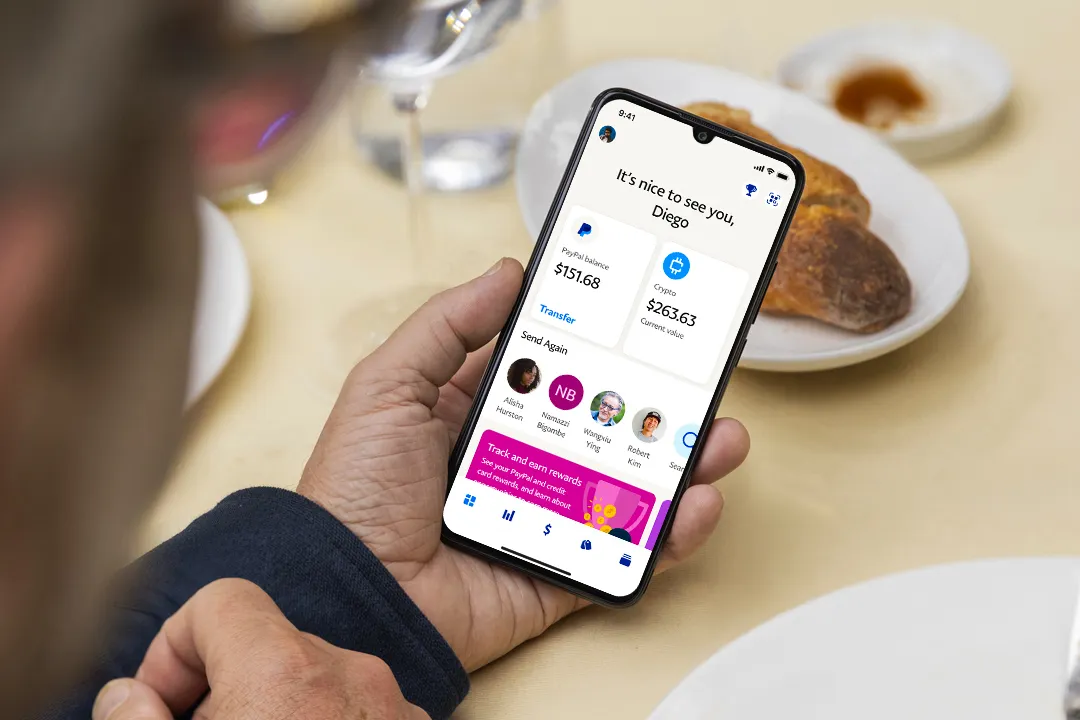

Beyond payments, the digital wallet is a platform for commerce with software startup Badge trying to help brands expand their wallet presence.

By: Justin Bachman• Published March 3, 2026

Beyond payments, digital wallets from Apple and Google traditionally haven’t done much.

In the future, however, wallets are likely to become commerce platforms where consumer brands extend their loyalty and marketing pitches far more than they do today, said Eric Senn, the co-founder and CEO of Badge, a software startup that offers infrastructure for companies to interface with wallets.

Wallets will “become more and more dynamic,” Senn said Monday in an interview. “We’re still kind of in that phase where you’re taking physical loyalty cards and gift cards and we’re digitizing them. But within that digitization, there’s this huge opportunity for things to become alive and more dynamic, truly interactive for the customer.”

Atop increasing wallet use for payments, Americans are also diversifying their wallets to house an array of identification and other digital needs: Drivers licenses, concert and sports tickets, passports loyalty cards and airline boarding passes.

Badge, based in San Francisco, was founded in 2023 and calls itself “the operating platform for mobile wallets.”

Badge customers use its technology to enable wallet push notifications, real-time updates and geofencing, so the phone wallet knows where you are and merchants can automatically drop pitches to the wallet. “If you have a loyalty card, you pull into a parking lot, you get an offer that pops up in the wallet,” Senn said.

Last month, Badge announced that it had raised $13.8 million from a series of investors led by Atlanta-based venture capital firm TTV Capital, with others including payment processor Stripe, Synchrony Ventures and Infinity Ventures. The capital raise brought Badge’s total funding to date to $17.1 million.

Lynne Laube, the co-founder and former CEO of Cardlytics, an advertising platform, and a partner at TTV Capital, will join Badge’s board of directors as part of the firm's investment.

Badge maintains “a very close relationship” with Apple and Google and formal contractual partnerships with both companies through which it offers customer feedback, Senn said.

Both tech giants offer guidelines on what functions can and can’t be done within their wallets and listen to feedback and suggestions from merchants about changes they’d like to see, Senn said.

“And then we go to Apple and Google and we’re like, ‘hey, just so you know, this is the feedback we're getting,’” he said. “And sometimes they implement it, sometimes they don't. It’s a little bit of a push and pull.”

Badge’s customers include Carrefour Group, the European grocery and retail giant; HOKA, a footwear brand owned by Deckers Outdoor; and Shift4 Payments, the large point-of-sale merchant services provider with a major sports venue business. Badge declined to disclose how many customers it has.

Instead of sending customers email, Carrefour can now put offers into customers’ wallets as they drive into a store parking lot, Senn said. “It’s just kind of using the existing programs and extending them into a much more preferable channel.”

Badge focuses on three of the most popular U.S. wallets — Apple, Google and Samsung — although the latter accounts for less than 1% in Badge’s business, Senn said. For businesses, this trio presents a challenge because each wallet is technically unique “and the wallets are constantly changing and evolving,” he said.

“That's why we built this infrastructure layer that gives companies a single entry point into the wallets and allows them to build a lot faster, and it also allows them to do more.”

Badge earns money through a software access fee for its platform and a fee for each push notification a customer wants to send to the wallet, similar to the charges retailers pay for sending their customers SMS text notifications, Senn said.

Wallet innovations from Badge and others are likely to come as virtual cards also delve more deeply into personalization, with new technical capabilities from fintech card issuers.

Mike Milotich, the chief executive of Marqeta, a digital card issuer and embedded finance company, predicted Monday that consumer loyalty programs will become a natural fit for personalized offers via cards.

“If you and I have the same credit card today we get the exact same reward,” he said at the Morgan Stanley Technology, Media and Telecom Conference in San Francisco. “We don’t think that’ll be the case in the future. Everything else is personalized and customized in technology and we think that’s going to come to card.”

Artificial intelligence “will take it to the next level” to adjust in real-time and to craft unique consumer offers via cards, Milotich said.

Article top image credit: Getty Images

Digital wallet use outpaces regulators

Consumers are increasingly turning to these mobile tools for convenience and new features, and regulators are trying to catch up.

By: Justin Bachman• Published Dec. 3, 2025

Back in 1999, eight years before Apple’s first iPhone release, a Silicon Valley software startup named Confinity introduced what it called a new “killer app.” It was dubbed PayPal.com.

The service allowed the “beaming” of funds between users, with only an email address. “Beaming Money by Email is Web’s Next Killer App,” Confinity said in its press release pitch, describing the technology.

The money-by-email effort arose from an earlier Confinity concept to transfer funds using infrared beams. The company demonstrated its payment feat by transferring $3 million with Palm Pilot devices in a breakfast display dubbed “Beaming at Buck’s” in the summer of 1999 at Buck’s, a Woodside, California restaurant. Max Levchin, the startup’s co-founder, recounted the story several years later in a talk at Stanford University with his Confinity co-founder, Peter Thiel.

A quarter century on, what began as a pioneering effort to encrypt money and move it digitally has morphed into a global payments industry anchored at the consumer level with digital wallets worldwide on billions of mobile phones. The mobile wallet has become standard for many consumers, some of whom consider a plastic payment card as outdated as a landline phone.

Regulators are still struggling to catch up with financial technology innovators. While the Biden administration tried to impose new oversight on big tech providers of digital wallets and peer-to-peer payments — such as Apple, Google and PayPal Holdings — the Trump administration has reversed that regulatory course.

Ages removed from the era of email payments, today’s digital wallets serve an extensive menu of functions: they now can carry a digital passport and driver’s license; store concert tickets and cryptocurrency; trade stocks; enable lending; allow paycheck deposits; and hold virtual credit and debit cards that can tap rewards currency.

The wallets also, of course, provide payment at physical stores and online. Meanwhile, financial technology companies like Cash App parent Block and PayPal are expanding the wallets’ feature sets to attract new customers.

PayPal leads the mobile wallet pack

Question in third-quarter: Which payment services have you used in the past 12 months?

More than three-quarters of Americans (77%) surveyed used at least one of the three most popular U.S. wallets — PayPal, Cash App and Apple — during the third quarter, according to data from Statista, which surveyed about 60,000 U.S. adults online, ranging in age from 18 to 64.

On average, U.S. consumers made 11 monthly payments with their phones last year, compared to four in 2018, the Federal Reserve found in its annual survey of payment methods. “Households earning less than $25,000 per year and adults 55 and older relied more on cash than other cohorts,” the May Fed report said. “In contrast, adults aged 18 to 24 were more likely to pay with a mobile phone, using their phones for 45% of all payments.”

Globally, about 4.5 billion people use a digital wallet today, with the number expected to grow to six billion by 2029, according to a November report from Juniper Research.

Precise U.S. wallet usage figures are difficult to determine. Apple and Google, for example, group their wallet revenue figures within larger categories of sales, such as services and subscriptions, and neither releases user numbers. Block, however, discloses Cash App’s user growth by releasing the number of monthly active users.

User and financial data for the largest digital wallets is difficult to ascertain as most companies group the information into larger sales categories.

Courtesy of PayPal

The “larger participants” rule

Lacey Aaker

Permission granted by Lacey Aaker

After analyzing the rapid growth of digital wallets, the CFPB in the Biden administration adopted a far more expansive view of what kind of guardrails were necessary for the industry. It followed through with a new rule boosting oversight of big tech companies that offer digital wallets in hopes of better safeguarding users.

Digital wallets are “doing a lot of bank-like activities, but their regulation is different from banks,” Lacey Aaker, a former CFPB policy analyst who worked on the now-defunct rule, said in an interview, noting the bureau’s rationale.

Many people use wallets and feature-rich financial apps as their primary source of banking. They don’t read deeply into companies’ disclosures about which funds may have federal deposit insurance or which debit payments are covered by the Electronic Funds Transfer Act, said Aaker, now a policy analyst with the nonprofit Consumer Reports.

“When we think about the everyday consumer, they don’t have time to read through all of the fine print,” she explained. “They have lives and jobs.”

In November 2023, the CFPB proposed a rule — “Defining Larger Participants of a Market for General-Use Digital Consumer Payment Applications” — to address the perceived problems within the burgeoning financial technology industry.

“Big Tech and other companies operating in consumer finance markets blur the traditional lines that have separated banking and payments from commercial activities,” the bureau said in a press release announcing the rule. The bureau concluded that “this blurring can put consumers at risk, especially when the same traditional banking safeguards, like deposit insurance, may not apply.”

The bureau’s final rule, which was rolled back earlier this year, would have extended supervision to seven “nonbank firms” that processed at least 50 million consumer transactions per year or about 98% of the 13.5 billion consumer payment transactions.

The CFPB did not identify any specific companies that would have been covered, nor did it include cryptocurrencies such as stablecoins within the rule. In December 2023, the bureau declined to reveal wallet data to Payments Dive under a Freedom of Information Act request, citing an exemption in the law for privileged and confidential information.

Nonetheless, the names surfaced this year when Congress moved to reverse the Biden-era CFPB rule. The Congressional Review Act resolution that overturned the regulation cited the seven largest digital wallet providers, namely Google, Apple, Samsung, PayPal and its Venmo unit, Block’s Cash App and Meta’s Facebook.

The goal was “really trying to sort of figure out what is the right amount of regulation for these types of apps and these types of platforms, that has consumer protection that doesn’t stifle innovation,” Aaker said.

Most critically — to the industry’s indignation — the bureau aimed to impose supervisory examinations of nonbank technology behemoths’ operations, much the way regulators oversee banks.

Tech companies and retailers including Apple, Etsy, Google and Netflix vehemently opposed the rule, which took effect in January 2025, weeks before the incoming Donald Trump administration. The tech firms filed a federal lawsuit to block the rule and lobbied lawmakers to rescind it under a congressional resolution, which passed and Trump signed in May.

The rule was a case of the bureau “getting over its skis,” said Jonathan Pompan, a Washington attorney with the law firm Venable, who advises financial services firms.

“It was trying to retrofit legacy consumer credit laws onto modern payment technology,” Pompan said. “And Congress recognized the mismatch and pulled the plug, while at the same time the administration was effectively placing [the CFPB] on life support.”

Protesters gather outside the Consumer Financial Protection Bureau on February 12, 2025 in Washington, D.C. The Trump administration has sought to dismantle the CFPB under Acting Director Russell Vought.

Kent Nishimura via Getty Images

A regulatory smorgasbord

Laura Huntley

Permission granted by Laura Huntley

Digital wallets operate under a patchwork of state and federal laws, including their relationships with banks for deposit insurance on customer funds and obligations to consumers under the Electronic Funds Transfer Act and Regulation E, said Laura Huntley, a managing director with FTI Consulting and a former banking regulatory attorney.

Banking regulators, the CFPB and the Federal Trade Commission also monitor financial firms for compliance with unfair, deceptive or abusive acts or practices, known as UDAP laws.

The states monitor money senders under their money transmitter licensing rules, with enforcement powers. Many of the activities within wallets are also monitored by the Treasury Department’s Financial Crimes Enforcement Network for compliance.

Wallet and P2P companies are “highly regulated,” said Miranda Margowsky, a spokesperson for the Financial Technology Association, which counts PayPal and Block as members.

The firms are “directly regulated” by states as licensed money transmitters and their bank partnerships fall under the purview of federal supervision, she said. Wallet companies also are subject to several U.S. consumer protection laws, Margowsky noted.

Despite the death of the CFPB’s larger participant rule, “I don't think we could ever say wallets weren’t really regulated,” Huntley said in an interview. “They have been regulated and will continue to be regulated under exactly the same messy regime.”

“Even if the rule had gone into effect, the existing federal and state frameworks would have remained fully intact,” she added. “What we would have been doing there is just adding another supervisory layer on top of something that’s already pretty dense.”

The bureau under former CFPB Director Rohit Chopra was “so aggressive,” she said. “We’re definitely seeing the pendulum having swung,” in terms of the bureau under Trump, Huntley said. “I think we got to a point there for a second where we said no risk was acceptable. And that’s crazy, because we’re in business.”

Currently, the bureau lists a dozen financial service areas where consumers may lodge a complaint, including with respect to “money transfers, virtual currency and money services.”

Beyond consumer payment services, the CFPB itself is facing critical questions about its future.

In November, the bureau said that the Justice Department had determined its quarterly funding mechanism from the Federal Reserve System was illegal and that its existing budget would lapse by early 2026. The agency also transferred its litigation and other legal enforcement work to the Justice Department, according to multiple media reports, some of which included reporting on plans to furlough most remaining CFPB staff.

Huntley and others pointed to the role that state attorneys general will increasingly play in consumer financial enforcement in the CFPB’s absence.

“I know we’ve been threatening this for a long time, but the states, they are coming,” Huntley said, noting that many former federal regulators at agencies like the CFPB and Office of the Comptroller of the Currency have moved into state roles.

Consumer trust and market policing

Unlike many developing markets such as Brazil, China and India, the U.S. has a long history of debit and credit card use, which in many ways has slowed the development of full-service financial wallets and their regulation, said Raynor de Best, a financial services analyst with the Hamburg, Germany-based market research firm Statista.

Emerging markets “skipped” the credit-and-debit era and designed payments around mobile wallets, said de Best, who studies the digital wallets market. “They wanted to push financial inclusion and they built the (payments) system along with the regulation at the same time,” he said.

Josh Istas

Permission granted by Josh Istas

Wallets and other payment platforms are deeply invested in safe products and competent customer service because of the financial consequences of shoddy products and trouble for their consumers, said Josh Istas, head of product for The Strawhecker Group, a financial services consulting firm.

“If that trust is abused in any way, shape or form that is against their major objective of growing their platforms,” Istas said. “There’s incentive from reputable good actors to ensure consumer protections.”

Google maintains dialogue with regulators, policymakers and industry partners to promote consumer protections given the growth of digital wallets, a Google Wallet executive, Dong Min Kim, said in an email from the company. Google also believes that the industry needs consistent regulatory frameworks to foster trust and innovation, he said.

Recent changes at Cash App — incorporating digital currencies and lending to a broader group of customers — are meant to respond to customer demands reflecting “how they participate in the modern economy,” Owen Jennings, Block’s business lead, said Nov. 13 during a product release event.

“Cash App is on this journey from what used to be a simple peer-to-peer app into what’s now a full-fledged financial platform that can allow a customer to run their financial life,” Jennings said. “The level of trust that’s required in order to cross that chasm is much higher.”

Apple and Samsung did not respond to several requests for comment; Block, Google and PayPal declined requests for an executive interview.

Block’s Cash App is one of the few wallets that publicly touts its growth, with 58 million active users in September 2025.

Block’s Cash App is one of the few wallets that publicly touts its growth, with 58 million active users in September 2025.

The wallets and apps ecosystem “has evolved to that point where companies who are offering digital banking need to become a bank to really fall into the framework that makes most sense for the service they’re offering,” contended Kyle Rosen, head of Americas for Thunes, a Singapore cross-border software firm with U.S. customers that include MoneyGram International and Western Union.

“The industry generally leads the regulator in terms of what occurs,” Rosen noted. “There’s innovation and then we need to regulate around it.”

Consumers are unaware of details such as the differences between a bank and fintech or which kinds of funds movements are covered by the Electronic Funds Transfer Act, said Tony DeSanctis, a senior director at Cornerstone Advisors, a bank consulting firm.

Some of the larger wallet risks for consumers revolve around which fintechs or neobanks enter the market, DeSanctis said. Ultimately, it will be about how responsibly new players act.

Article top image credit:

Thomas Trutschel/Picture-Alliance/DPA/AP

Apple sets sights on travel spending

The tech company is embedding its digital wallet as a method of payment at many stages in the travel process in a bid to attract more consumer use.

By: Patrick Cooley• Published Nov. 5, 2025

Apple wants to make its digital wallet an indispensable part of payments for travel, according to a company executive who spoke at an industry conference last week.

The tech behemoth aims to have travelers use its digital wallet at numerous points on their journey, said Jennifer Bailey, vice president of Apple Pay and Apple Wallet. The firm has embedded Apple Wallet as a payment method at airports, hotels and in public transit systems, Bailey said.

In some cases, travelers can download their airline boarding pass to Apple Wallet and use an ID stored on the app to get through Transportation Security Administration checks, she said during a question-and-answer session at the Money 20/20 conference in Las Vegas on Oct. 26.

But the use of the digital wallet can start even before arriving at the airport, she said. “If you’re like me and you live in the suburbs, you probably drive a car,” Bailey said. “I use a tap to unlock my car with a digital key that’s in my Apple Wallet.”

Users of the digital wallet can also use Apple Pay to ride public transportation in 800 cities, she said.

Cafe and restaurant chains like Starbucks, which are common in airports, also accept Apple Pay, as do ride-share services like Uber and Lyft, along with many hotels, Bailey said.

Apple Pay is the payment service that lets Apple Wallet users make transactions with credit cards stored on their digital wallets.

The tech giant has in recent years delved deeper into providing wallet services for airline travel needs. American Airlines, for example, announced last month that it would let travelers add a boarding pass to their Apple Wallet, and Alaska Airlines started accepting Apple Pay for in-flight purchases in 2023.

To be certain, the tech company faces an uphill battle in its quest to expand travel payments as large banks and their airline and hotel partners dominate travel spending.

Competitors like card company American Express as well as the bank card issuers Capital One Financial and JPMorgan Chase see hundreds of billions of dollars spent through their payment products each year.

American Express, for example, reported $376 billion in travel spending on Amex cards so far in 2025, Forbes reported in September. Meanwhile, the card network Visa – which has co-branded credit cards with airlines like Southwest and United – saw between $920 billion and $1.2 trillion in estimated travel and entertainment spending for the year, the news outlet said.

Apple has not disclosed in recent earnings reports how much consumers spend on travel through its digital wallet. Company spokespeople did not respond to a request for information on how much Apple users spend on travel-related purchases.

Article top image credit: Courtesy of Apple

US consumer trust in digital payments lags globally

Consumers in the U.S. are less trusting than those in other countries when it comes to using digital tools to make payments, according to a fintech study.

By: Tatiana Walk-Morris• Published Aug. 22, 2025

Dive Brief:

Only 8% of U.S. consumers engage in online transactions every day, versus 35% in Brazil and more than 20% in several countries, including Saudi Arabia, Japan and United Arab Emirates, according to the results of a study by the survey firm YouGov and the London-based fintech Checkout.com.

While nearly all of China’s consumers (93%) have adopted a digital wallet for making payments, and 80%, or more, of the populations in Saudi Arabia, Brazil, Egypt and the United Arab Emirates have, only about two-thirds (65%) of U.S. consumers have downloaded such apps, according to results of a survey for the study by YouGov.

Meanwhile, a quarter of China’s population uses digital wallets to make peer-to-peer payments every day, and a fifth of consumers in Brazil do the same, but only 9% of Americans use the tool daily, according to a survey of 18,000 adults across 16 countries. The study didn’t provide information on how or when the survey was conducted.

Dive Insight:

The report from Checkout.com and YouGov sketches out the global differences in trust levels for using digital payment tools and engaging in online checkouts. Compared to other regions, European and North American consumers tend to exhibit more skepticism when it comes to e-commerce transactions than consumers in other parts of the world, the study suggested.

While the study was initially issued in May, Checkout.com highlighted the global disparities in an Aug. 13 press release. Major providers of digital wallets in the U.S. include Apple and Google, though they are typically linked to consumers’ credit cards, debit cards or bank accounts.

The top reason that U.S. consumers said they were short on trust in using digital payments for commerce was that they are uncertain about the safety of the checkout. Nearly half (46%) of U.S. consumers expressed that uncertainty. That was the same reason for concern with consumers in 11 of the 16 countries, with the percentage being about the same in most of them.

The top reasons for concern in the other five countries related to the ease of use and the lack of a preferred payment method offered.

Part of the mistrust for U.S. consumers may be related to half of them reporting they have been a victim of fraud when using their cards for payments (the study wasn’t clear about whether it was credit or debit cards). Still, consumers in Brazil reported even higher levels of card victimization (53%) and the percentage in the United Arab Emirates was the same as in the U.S.

And even though they have very different digital payment use rates, consumers in the U.S. and China were nearly equally nervous about storing their card data on an e-commerce site, with that being the case for 43% in China and 42% in the U.S.

Checkout.com’s report echoes other research suggesting that card fraud remains a problem for consumers and payment providers alike.

A Nilson report released earlier this year projects that fraud losses in card payments will reach $403.88 billion over the next decade. Meanwhile, 73% of financial institutions surveyed by the Federal Reserve Financial Services said debit cards were the top payment method for fraud attempts in 2024.

Peer-to-peer payments are also a hotspot for fraudsters. An AARP survey released last year found that about a fifth of adult peer-to-peer payment users have been an “intended victim” or a victim of “financial exploitation.” Of those targeted for scams, four in ten lost between $101 and $1,000, the survey of 2,014 adults found.

Article top image credit: Alamy

Paze aims to pump up the volume with Fiserv

The digital wallet owned by seven banks has loaded 150 million customer cards onto the system. Now, it’s working with its processor ally to add more banks.

By: Lynne Marek• Published April 29, 2025

Dive Brief:

Paze, the digital wallet launched last year by Early Warning Services, has loaded 150 million debit and credit card accounts onto its nascent system, according to an EWS presentation at Nacha’s Smarter Faster Payments Conference. Now, those bank customer card holders can opt into the wallet if they’re interested in using it.

More big banks are expected to link to Paze later this year, Early Warning’s Chief Partnership Officer Eric Hoffman said Sunday during a panel discussion at the conference. He spoke alongside Deva Annamalai, Fiserv’s head of client strategy and solutions for digital payments. The processor is partnering with EWS to attract more banks to offer the digital wallet to their customers for online purchases.

With Fiserv, there is “exposure to thousands of banks,” Hoffman said in an interview after the panel discussion, explaining how additional banks will disclose working with Paze as they announce that the service is available to those banks’ customers.

Dive Insight:

The latest card count is up from 125 million cards connected last October. Early Warning Services has been eyeing the 150 million card goal for some time because the accounts belong to customers of EWS’s bank owners, but now it will set its sights higher, to add more card credentials.

As Fiserv helps bring its bank clients onto the Paze system, it will benefit from the increased transaction volume it processes through the digital wallet.

Scottsdale, Arizona-based Early Warning Services has been building the Paze system since at least 2022, with a slow roll-out to its bank owners since its launch last September.

The seven major banks that own EWS are Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank and Wells Fargo. Those EWS banks also developed the bank-to-bank payments system Zelle, which sent $1 trillion between users last year.

Paze got a lift last year after the arrival of a new leader, Serge Elkiner, who was tapped to become its general manager. Hoffman is also somewhat new to the project, having arrived just as Paze was launching last year. He’s bringing experience from his work as a business development executive for Apple Pay.

Some 70% of U.S. consumers don’t use a digital wallet so there is a broad opportunity to attract new users without having to do battle with some of the long-time rivals in the field, namely Apple Pay and PayPal, Hoffman said. “They may use their card on file (online), but they're not using digital wallets – this is the consumer that we're going after,” he explained.

Paze will be directed at consumers between 35 and 65 years-old who tend to be wealthy, and have been “protectionist” in their thinking about digital wallets, Hoffman said. This group has generally avoided using digital wallets so far, but they’re likely to sign up for Paze if it’s offered by their banks, just like they did with Zelle, he said.

“Consumers trust their banks – that’s what we’re hanging our hat on,” he said.

When asked why it’s taken so long to get the system rolled out, Hoffman suggested it was simply time spent developing the Paze technology. He conceded during the discussion that the Paze team is “still closing some technical gaps.”

He also noted that getting bank card issuers up and running with Paze at the same time EWS was trying to add merchants to the system was no easy task.

Merchants offering the Paze payment option to their customers so far include retailers Sephora and Fanatics. Hoffman expects Paze will also add more merchants to the online Paze shopping ecosystem later this year.

Article top image credit: Getty Images

Inside the rise of digital wallets

Even as some parts of the world rely on digital wallets for payments online and in-person, consumers in the U.S. are still getting used to the idea. As more competitors enter the market, offering fresh features to attract consumers, use of digital wallets in America is poised to grow too.

included in this trendline

Apple, Google wallets get personal

Digital wallet use outpaces regulators

Apple sets sights on travel spending

Our Trendlines go deep on the biggest trends. These special reports, produced by our team of award-winning journalists, help business leaders understand how their industries are changing.